1. WHY ARE MARKETS RISING, DESPITE COVID AND ECONOMIC HEADWINDS?

-

Financial markets tend to be forward looking and optimistic in terms of valuing for a security’s future potential. Therefore many times near term headwinds are looked through for longer term potential.

-

Significant central bank and government support through monetary (low interest rates and asset purchases) and fiscal (stimulus) policies have injected trillions of dollars into the economy, much of which have led to the rise of asset prices, including the financial markets.

-

The anticipated benefits of a recovery in the economy as it reopens this year, and both current and expected government stimulus as meaningfully increased growth expectations for 2021.

-

There are some seasonal factors in which the markets and company earnings expectations tend to be positively supported in the first half of the year due to optimism, which if do not fully come to fruition can lead downgrades towards the end of the year.

-

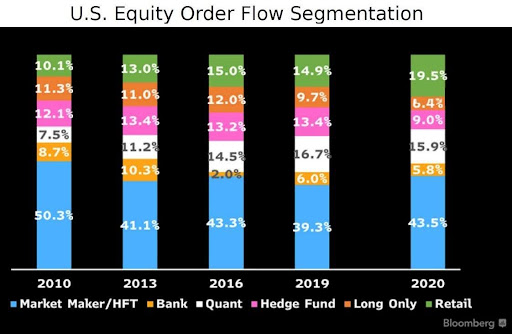

One underappreciated factor is the meaningful rise of investors and investment products that don’t consider traditional valuation metrics. For example, the equity trading market share has gone away from traditional funds and continues to shift towards individual (aka retail) investors, computer-driven models, and ETFs. (See chart below)

2. WHAT COULD CAUSE MARKETS TO DECLINE?

There are an unlimited number of factors that could cause a market to decline, but some of the general concerns for US equity markets to consider in 2021 are below:

-

Rising US interest rates, particularly maturities of 5 years or longer (as the Fed is intent on keeping short term benchmark rates close to zero for the foreseeable future).

-

Meaningful rise in inflation, particularly in the second half of 2021, going into 2022, as this may force the Fed to raise short term interest rates quicker than currently expected.

-

Meaningful reduction, and even reversal of, central bank asset purchases.

-

An unknown/unexpected event (ex: COVID) in which investors and computer models can’t quantify. We saw the severity of such events in March of 2020.

-

Inability to adequately manage COVID spread or vaccination, leading to extended shutdowns.

-

Change in tax policies, or investment regulation, that could lead to higher tax rates or costs for individuals or companies.

-

Continuation of elevated unemployment levels for an extended period of time.

-

Political and geopolitical risks.

-

Recognition of excessive valuations for individual stocks and the overall market.

-

Forced deleveraging whether driven by banks, brokers or regulators. The events of the Jan short squeeze (ex: GameStop) and Mar Archegos unwind have put significant pressure on all financial parties to review and consider reducing leverage in the system.

As of now, we believe the overall market optimism that continues will face additional headwinds in the second half of the year and going into 2022. Specific concerns include rising inflation, interest rates, tax rates and regulations.

3. HOW SHOULD I APPROACH INVESTING IN 2021?

We believe traditional buy & hold or 60% equity/40% fixed income strategies will no longer meet most investors return or income needs going forward, as they may have in the past. Considering current market valuations, volatility and stage in the economic cycle, investors need to be more tactical and open up their purview across asset classes and geographies. This can be realized by conducting the right type of fundamental research or partnering with financial professionals who can help achieve your investment goals.

4. TESLA - JOIN THE RIDE OR GET OUT BEFORE A POTENTIAL CRASH?

The debate on TSLA is one of the most popular amongst investors today. Essentially you are either a believer in the long term potential of this company retaining leadership in the areas of EVs, batteries, autonomous driving and solar or you believe the stock is overvalued and that will eventually be recognized by the market.

There is an endless amount to read on TSLA stock so below we tried to highlight some differentiated points to consider:

What got us to the stock price today:

-

In December 2019 the stock started to move out of the range it had been in for the previous six years.

-

About 150M shares of shorts covered over the past 18 months, which represents 20% of today’s free float.

-

Analysts started factoring in the next leg of production growth as visibility on output grew.

-

Achievement of Musk’s incentive compensation plan based on revenue and market cap targets was an underlying factor.

-

Inclusion into the S&P 500.

-

Strong demand from institutional and individual investors for innovative and ESG friendly stocks.

PROS:

-

Any of their ancillary businesses (solar, storage, commercial vehicles, autonomous, etc) develops visible revenues in the foreseeable future.

-

Ability to monetize their data and first mover advantage.

-

Ability to retain global EV market share despite rising competition.

-

Growth in non-US markets continues to grow above expectations.

-

Their production capacity grows faster than anticipated.

-

Demand for EVs remains above supply for the foreseeable future.

-

Continued benefit from ESG theme.

CONS:

-

Unless additional businesses aside from their current passenger vehicles come to fruition their current valuation is expensive on most metrics.

-

Competition in EVs is only set to rise as most major auto manufacturers, along with many startups, globally are ramping up production. Arguably the major established auto firms will be able to provide better maintenance and service to customers than TSLA has thus far.

-

Potential of meaningful pull forward of reported financials to achieve Musk’s incentive bonuses and TSLA inclusion in the S&P 500, which could catch up to them over the coming quarters.

-

Delays in their supply chain, from semiconductors to batteries, could lead to lower production growth relative to expectations. Most other auto manufactures are currently facing this headwind in 2021.

-

Their Berlin facility will continue to face headwinds and delays, which are not currently fully factored in. Keep in mind Volkswagen is making a meaningful push into electric vehicles and have political pull in Germany.

-

Their production expansion into China will prove difficult and even backfire over time. While the market is mostly viewing their foray into China as a positive, it’s worth noting most foreign companies have a difficult time operating in China without having their intellectual property replicated by local companies over time. China arguably could become the leader in EVs and in that scenario it’s likely they would utilize western technologies as they have in most other industries.